Medigap

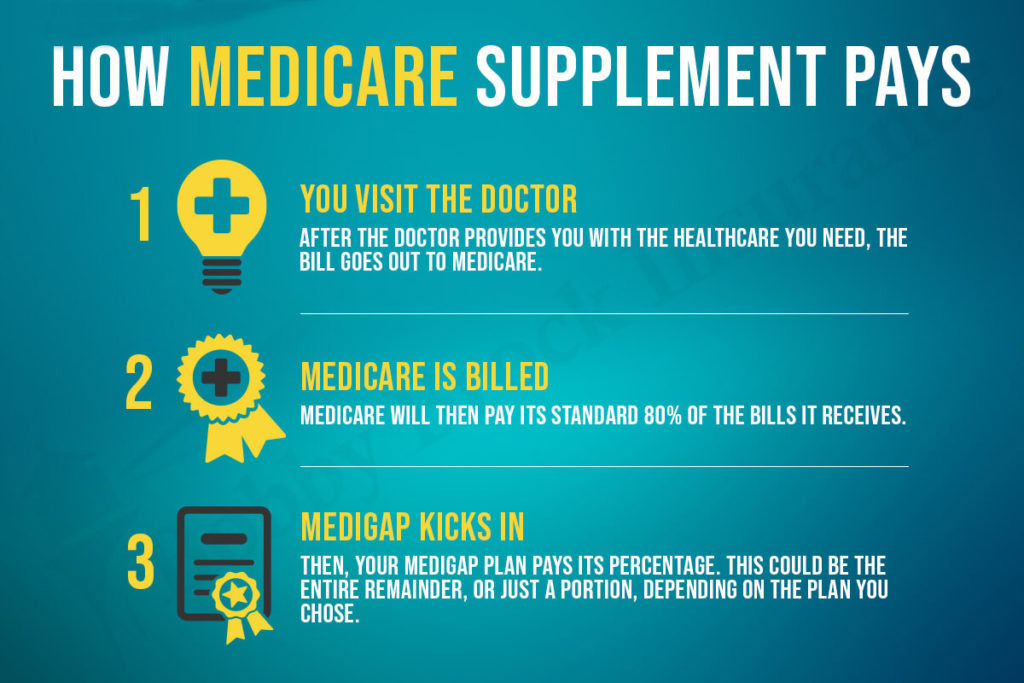

Medicare Supplement plans, also known as Medigap, are policies that help pay for the excess charges left over by Medicare. These costs are things like your deductibles and coinsurance.

Medicare Supplements Users’ Guide

This guide can be helpful if you’re considering buying a Medigap policy or already have one. It’ll help you know how Medicare Supplement plans work.

What is Medicare Supplemental Insurance?

Medicare Supplement plans, or Medigap, are insurance policies sold by private insurance companies that are licensed to sell Medicare plans. They help you pay for out-of-pocket costs for services covered under Medicare Part A and Part B. These costs include deductibles, coinsurance, copayments, hospital costs after Medicare pays its share, skilled nursing facility costs, and more. Some Medicare Supplement insurance plans even include coverage for medical services while traveling outside the United States.

What are the different plans?

Different Medicare Supplement plans are labeled with a different letter between A through N.

Medicare Supplements feature different benefits. However, each plan must have the same standardized coverage no matter which insurance company you purchase the plan from.

Which Medicare Supplement plan should I choose?

Some Medicare beneficiaries want a plan that covers everything so they don’t have to worry about out-of-pocket expenses. Others simply want some of their deductibles and copays paid for but are mostly worried about low premiums. Ultimately, the choice is up to you.

Which Medigap policy has the highest coverage?

Medicare Supplemental Plan F has the highest level of coverage. It pays for all of your cost-sharing on covered services so you have no out-of-pocket expenses.

Medicare Supplemental Plan G is the second-best in terms of coverage. The only thing not covered is that you still pay the Part B deductible once per year. This keeps your Medigap premium lower and, in turn, may save some beneficiaries some money in the long run.

When can I enroll in Medigap insurance?

Once you have Medicare Part B, you have six months to enroll in a Medicare Supplement plan with no health questions. This is a one-time open enrollment in which you cannot be turned down for any health conditions, you cannot be asked any medical questions, and you cannot be charged an additional premium for health reasons.

However, once this one-time enrollment is over, insurance companies can begin to refuse you based on health.

This is why open enrollment is an important time to remember.